Choosing a bank with digital services for saving requires considering legality, fees, ease of transactions, and transparency of information. With more banks offering app-based services, it is important for prospective customers to understand the key factors before opening an account.

Today, almost all banks provide digital services. However, not all offer the same fee structure, features, and level of convenience. Here is a guide you can use.

1. Make Sure the Bank Is Licensed and Supervised by OJK

Legality is the most important factor.

Choose a bank that:

-

Is licensed and supervised by the Financial Services Authority (OJK)

-

Is registered as a participant of the Indonesia Deposit Insurance Corporation (LPS)

Banks under regulatory supervision must comply with banking regulations, including fee transparency and customer protection. Deposits in LPS-participating banks are insured in accordance with applicable terms and coverage limits.

To verify whether a bank is licensed and supervised by OJK and registered with LPS, visit the official OJK Bank Data and LPS Participating Bank pages.

2. Check Administrative and Transaction Fees

Registration fees, monthly administrative fees, and transfer fees can affect your savings growth and should be considered when choosing a bank.

Pay attention to:

-

Monthly admin fees

-

Initial deposit requirements

-

Interbank transfer fees

-

Minimum balance

-

Withdrawal fees

This information is usually available on the bank’s official website or on its fees and interest information page. Avoid choosing a bank based solely on promotions without reading the applicable terms and conditions.

3. Check the Ease of Access to Digital Services

A good digital bank should provide:

-

A stable mobile banking application

-

Online account opening process

-

Easy-to-use transfer and payment features

-

Real-time transaction history access

-

24-hour customer service that is easily reachable through official social media, phone, email, or in-app support

This convenience helps customers manage their savings without having to visit a branch office.

4. Review Transparency of Interest Rate Information

Savings interest rates vary between banks and may change according to each bank’s policy.

Things to consider:

-

Interest information is clearly displayed

-

No misleading claims

-

Terms and conditions are easily accessible

Savings interest is not the only factor. Also consider service consistency and the overall fee structure.

5. Choose a Bank with a Complete Service Ecosystem

A good digital bank generally provides:

-

Savings accounts

-

Transfer and QRIS features

-

Bill payment services

-

Financing products

-

Investment products

-

Loan products

A complete ecosystem makes it easier to manage finances within a single application.

6. Consider Comfort and Service Responsiveness

Beyond digital features, a bank should also provide:

-

Operational offices or branches in certain cities

-

24-hour customer support

-

Systems that support smooth transactions

Convenience is not only about the application, but also about reliable bank support when issues arise.

Example of a Bank with Digital Services

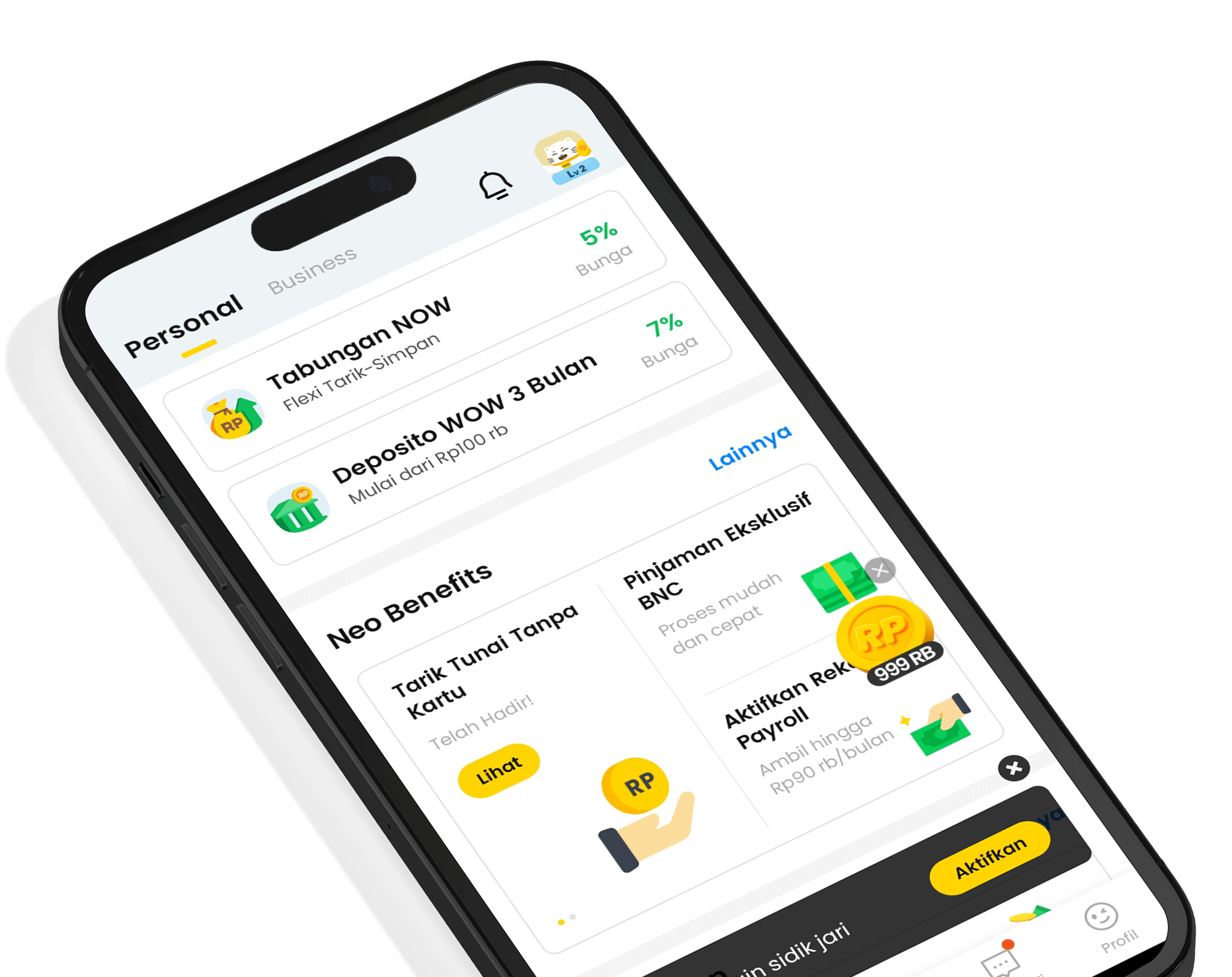

One example of a digital-service bank in Indonesia is Bank Neo Commerce, which operates through the neobank application.

This bank:

-

Is licensed and supervised by OJK

-

Is a participant of LPS deposit insurance

-

Provides digital banking services through the neobank application

Through neobank, customers can open accounts, save money, make transfers, pay bills, apply for loans, and access various banking products. Some of the features and products available in neobank include:

-

Regular Savings

-

NOW Savings

-

Neo Green Savings

-

WOW Time Deposit

-

FLEXI Time Deposit

-

Neo Loan

-

Neo Business

-

Neo Wish

-

Neo Gold

-

Mutual Funds

-

Cardless Cash Withdrawal

-

Bill payments and top-ups

-

Payment features: QRIS & Virtual Account

-

Social and digital transaction features

One of the available savings products is NOW Savings, which offers:

-

4.00% interest per year

-

Interest calculated based on daily balance and paid daily

-

No monthly admin fee as long as the account remains active. A Rp5,000 monthly fee applies if there is no login or transaction for 6 consecutive months

-

Funds can be withdrawn according to applicable terms without penalty

-

Suitable for emergency funds (3–6 months of expenses), urgent needs, and short-term targets (1–12 months)

Customers should always read the terms and conditions before using the NOW Savings product.

FAQ

1. What should be considered when choosing a bank with digital services?

Make sure the bank is licensed and supervised by OJK and is a participant of LPS.

Check transparency of fees, interest rates, and product terms.

Ensure ease of access to digital services and availability of financial features that support daily needs.

2. Can neobank be used for saving?

Yes. neobank offers several savings products such as Regular Savings and NOW Savings.

Regular Savings can be used for daily transactions.

NOW Savings offers 4.00% annual interest paid daily and no monthly admin fee as long as the account remains actively used.

3. Is Bank Neo Commerce legal and supervised by OJK?

Yes. Bank Neo Commerce is licensed and supervised by OJK and is a participant of LPS deposit insurance in accordance with applicable regulations.

***

Interest rate information stated is valid as of April 2, 2026.

For more information about other neobank products and services, visit the official website: https://s.id/bankneocommerce

Product and service information at Bank Neo Commerce can be accessed through the neobank application on the PlayStore or App StorePlay Store or App Store. Check the latest updates at https://s.id/fbtabungannow.

PT Bank Neo Commerce Tbk is licensed and supervised by the Financial Services Authority (OJK) and Bank Indonesia (BI), and is a participating bank of the Indonesia Deposit Insurance Corporation (LPS).

What are you waiting for?

Let's try neobank now!

.png)

.png)

PT Bank Neo Commerce Tbk is licensed and supervised by the Financial Services Authority (OJK) & Bank Indonesia (BI) and is a member of Indonesia Deposit Insurance Corporation (LPS).

The maximum deposit amount insured by LPS per customer per bank is Rp2 billion. To find out the LPS Guaranteed Interest Rate, please access here.

Copyright © 2023, All Rights Reserved, PT. Bank Neo Commerce Tbk

PT Bank Neo Commerce Tbk is licensed and supervised by the Financial Services Authority (OJK) & Bank Indonesia (BI) and is a member of Indonesia Deposit Insurance Corporation (LPS).

The maximum deposit amount insured by LPS per customer per bank is Rp2 billion. To find out the LPS Guaranteed Interest Rate, please access here.

Copyright © 2023, All Rights Reserved, PT. Bank Neo Commerce Tbk